The housing crisis keeps many young Americans up at night. Trump’s recent executive order claims to help Americans rest easier by excluding corporate interests from the housing market. But with a problem as complex as the housing crisis, will this be enough to solve the problem? And what is its root cause? Corporations buying up all the houses as Trump suggests? Lack of construction worsened by COVID-era supply shortages? Or maybe it’s the baby boomers driving up real estate costs? Let’s break it down.

The U.S. Chamber of Commerce states that “The housing crisis stems from a fundamental issue: the construction of new homes has failed to keep pace with demand, particularly in high-growth areas.” That sounds simple —- too many people, not enough homes.

But why have we not just built more? The Chamber of Commerce again offers two answers, overregulation, and high cost of construction materials. Overregulation makes the construction of new homes so time-consuming and expensive, often by design, discouraging development. In addition, smaller construction companies struggle to compete with larger ones. The result is existing homeowners, often older and wealthier, can regulate construction out of their communities, preventing the building of homes that might drive down property value and inflating the value of homes that are already owned.

If you do manage to cut through all the red tape, construction costs, which hit a 25-year high in 2022, exacerbated by COVID supply chain disruptions, prevent many from building rather than looking for an existing home.

Trump’s tariffs have only added to high prices. An NBC News examination in 2025 found that the cost of materials to construct a single-family home rose $4,405 from $86,516 to $90,921, due to tariffs placed on China and Canada. This figure is even more startling given it doesn’t include the price of labor, as the report’s consultant chief economist for the National Association of Home Builders, Robert Dietz added “About three-quarters of home builders right now are having difficulty pricing their homes for buyers because of uncertainty due to construction input costs.”

While these conditions make homeownership exclusionary, for many Millennials, Gen Z, and Baby Boomers have reaped the windfall. Despite being 19% of the population, boomers own about $85 trillion in assets, 51% of the total wealth in America. Much of this wealth is tied to homeownership. While your friendly neighborhood Boomer may say that this wealth is only a result of hard work and investment, economists interviewed by the Washington Post pointed to “…uniquely favorable economic conditions that occurred during their working lives…So much so that it would be difficult for younger generations to emulate, especially as they are more likely to be weighed down by debt or child care costs.” These conditions included wage growth, lower tuition, less taxation, cheaper health care, and most relevant to our discussion, cheaper housing prices. Between 1980 and 2025 the price of the median home went from $65,000 to $410,800. This means that while in their 20s boomers were able to buy homes, the average age buying homes today is around 40. So while Baby Boomers enjoy their home equity, younger generations have problems buying their own.

So is Trump’s big beautiful executive order going to fix these problems? In short, no. While kicking the special interests out of the housing market sounds great, only about 1% of the housing market is owned by big investors. If Trump does manage to do so he might be worsening the problem instead. According to a co-director at the American Enterprise Institute Housing Center, Tobias Peter, these investors serve “a vital function by fixing up dilapidated homes.”

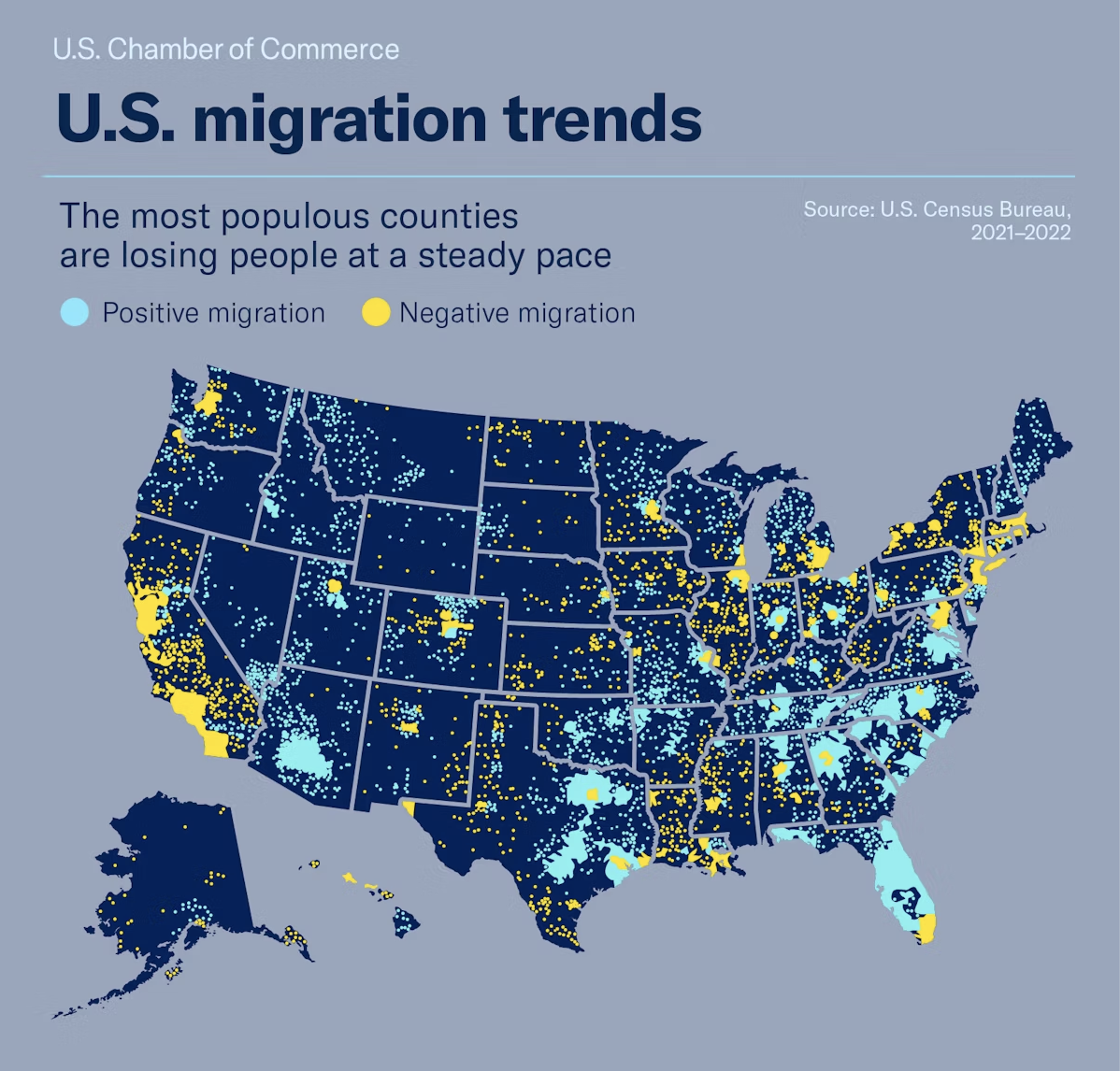

So how do we fix the housing crisis? In the short term, many Americans are moving from more expensive heavily populated areas in the Northeast and California to the South — shown in this graphic by the U.S. Census Bureau.

But this is an often difficult and expensive solution that has its own drawbacks. Americans are increasingly forced to make what Associate Professor of Landscape Architecture and Urban Planning at Texas A&M University, Ives Garcia, has called a choice between affordability and safety. While moving to the south may be cheaper, it often puts homeowners in areas that are more likely to experience extreme weather events caused by global warming. Simply moving to cheaper areas is not a reliable solution even for those who can afford to uproot their lives.

The housing crisis has no one cause, and won’t have just one savior. Trump’s executive order may look good to voters but fails to address the fundamental problems Americans are experiencing. If Trump is serious about real change he could lessen or remove tariffs on construction goods from China and Canada. The Federal Reserve can cut mortgage rates, giving Millennials and Gen Z a break. Baby Boomers can pass down their homes and loosen strict homeowners association regulations that make the construction of new homes prohibitive, as lawmakers should do at the state and federal level.

And those of us in Gen Z who have given up on ever owning a home, who, according to a paper by Northwestern University and University of Chicago researchers, are overspending, working less, and making risky investments, can reject the nihilistic thinking and give the American dream another shot.