In the House of Representatives, there was a bill on the docket titled, the Financial Services Racial Equity, Inclusion, and Economic Justice Act, promoted by Representative Maxine Waters. It advocates for more diversity, and access to the financial services industry1. Currently, the bill sits in the Senate’s “Committee on Banking, Housing, and Urban Affairs”; there are no updates on its status after this action.

Why is this bill so imperative? As capitalism becomes the primary vein of America’s economy and government, equity requires financial access.

Think back to the use of “red-codes” known as redlining, where maps were strategically drawn to deny services and investment in neighborhoods based on race. Sociologically, redlining habits have impacted places with a high population by depriving their communities of mortgage loans (and other capital) for decades. The first clause of the bill prohibits discrimination against applicants based on zip code and census tract. This will prevent the legacy of utilizing financial discrimination to marginalized minorities by revising how the financial industry evaluates zip codes and census tracts.

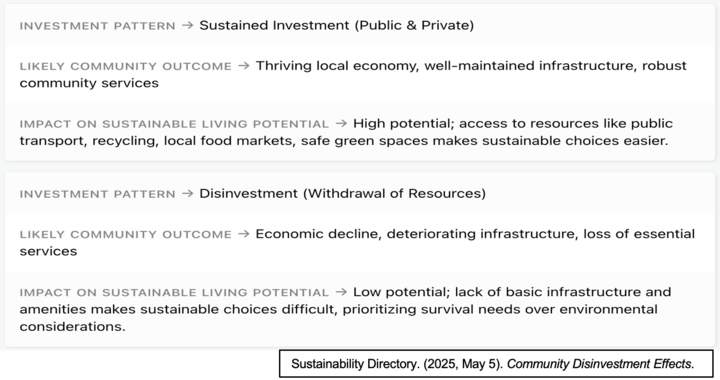

A major element that would correct practices like the above would be sustained investment in historically underserved communities. The data in the table below confirms the impact of disinvestment and defines how sustained investment strengthens communities’ local economy. Sustained investment is represented in the second clause of the bill, through requiring monetary reserves to set-aside funding for minority lending institutions. Allocating a reserve for minority lenders to distribute as they see fit, not only enables more personal loans to minority groups, but enables minority leaders to serve their community. On a larger scale, this would advance funding opportunities to support black-owned businesses, provide black student loans, and finally protect mortgage loan access for black home buyers.

We can currently gauge if this bill will truly 1) expand access to the financial service industry, and 2) promote the survival of local economies by visiting a cultural heritage city.

In my opinion, understanding that the context of Jewish Americans after WWII meant the removal of institutionalized antisemitism, you can witness how a shift in economic access enables their community to establish: Synagogues; Jewish-owned businesses with culturally specific foods, products, and goods; and parks & recreation that fulfill their culturally relevant needs and lifestyle. To broaden this topic I pulled information from Carmel Ullman Chiswick’s chapter, “How Economics Helped Shape American Judaism”, from The Oxford Handbook of Judaism and Economics, edited by Aaron Levine. The objective of this book is to detail the evolution of the Judaist religion in relation to American economics. However, Chiswick details that, while ‘the new world’ expanded financial access, it was only with the removal of antisemitism that caused a positive shift in Jewish economic positionality2, the result— culturally responsive financial freedom.

In context, governing lending agencies’ investment into black communities would enhance financial support towards infrastructure in their neighborhoods: black shopping centers, black parks & recreation, and other culturally relevant economic capital. This level of sustained investment will potentially generate a community circulated reserve economically mobilizing the “black dollar.”

Economic marginalization is a form of institutionalized racism. The Financial Services Racial Equity, Inclusion, and Economic Justice Act aims to rectify this by diversifying and prohibiting discrimination within the financial sector. In theory, legally mandating investment in underrepresented communities would establish equitable distribution of financial sector reserves. In connection with local Jewish economies, this theory is measurable, confirming that the “black dollar” can create a reality within the black community where economic marginalization transforms into economic independence.

Acknowledgement: The opinions expressed in this article are those of the individual author, not necessarily Our National Conversation as a whole

1The clauses within the bill establish access to credit, mortgages, and banking services by 1) prohibiting discrimination with respect to credit transactions on the basis of an applicant’s sexual orientation, gender identity, or location based on zip code or census tract; 2) establishing language translation requirements for residential mortgage applications; and 3) providing funding set-aside for minority lending institutions. After being voted on in the House, there was an amendment constituting, nothing prevents community banks from opening in underserved areas in relation to this Title.

2Chiswick states, “Although anti-Semitism was not completely absent”. . .”The United States presents an economic environment unlike any other in the millennia-long experience of the Jewish people. As the “Great Experiment” in democracy and religious freedom, America broke with its European roots in ways that greatly reduced the economic penalties imposed by society on Jews per se. American Jews were subject to no special taxes and faced no laws restricting their ability to choose an occupation, to own property, or to enforce contracts.”

Bibliography

Actions – H.R.2543 – 117th Congress (2021-2022): Financial Services Racial Equity, Inclusion, and Economic Justice Act. (2022, June 21). https://www.congress.gov/bill/117th-congress/house-bill/2543/all-actions

Chiswick, Carmel Ullman, ‘ How Economics Helped Shape American Judaism’, in Aaron Levine (ed.), The Oxford Handbook of Judaism and Economics, Oxford Handbooks (2010; online edn, Oxford Academic, 18 Sept. 2012), https://doi.org/10.1093/oxfordhb/9780195398625.013.0033, accessed 24 June 2025.

Community disinvestment effects → term. Lifestyle. (2025, May 6). https://lifestyle.sustainability-directory.com/term/community-disinvestment-effects/

H.R. 2543 (117th): Federal Reserve Racial and economic equity act. GovTrack.us. (n.d.-a). https://www.govtrack.us/congress/bills/117/hr2543/summary

H.R. 2543 (117th): Federal Reserve Racial and economic equity act. GovTrack.us. (n.d.-b). https://www.govtrack.us/congress/bills/117/hr2543/details